How Much Will Obamacare Cost Me? A Handy-Dandy Calculator

Try this handy-dandy calculator developed by Kaiser, hosted by NPR, on a post by Scott Hensley.

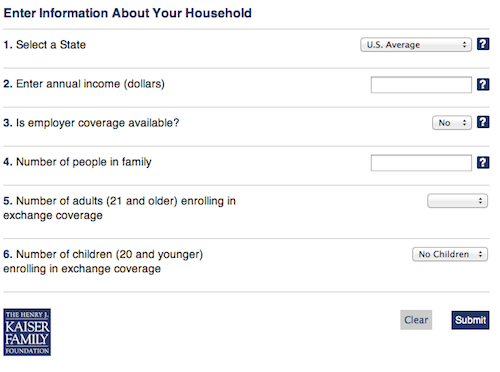

The calculator is live at the link, but here's a screenshot. If you post here anonymously and don't mind revealing your rate, please do.

If you post here anonymously and don't mind revealing your rate, please do.

via @Lifehacker

For 1 person, $3,198. I'll take the IRS penalty. Thank you Obama.

NoNameRightNow at September 30, 2013 1:53 PM

I had to cheat and say we didn't have coverage available through an employer to get anything but a big 'fuck you'. When I did, I ended up with an annual premium of $8,713 for our family of 5, with an available tax credit of $353. Thanks, but no thanks: we'll stick with the $312 per month for our employer-backed plan with a max out-of-pocket less than half that offered by the exchange plan, super low deductible, and dental and optical inclusive.

Jess at September 30, 2013 2:31 PM

I get insurance through my employer, but if I didn't this says insurance through an exchange would cost $7,910, and we are not eligible for any type of subsidy. I'm 32, the husband is 41, no tobacco, one child, in Texas.

I don't see on there what TYPE of plan it is- HMO? PPO?

Anyway, I'm glad I work for a big evil corporation with great benefits.

ahw at September 30, 2013 2:45 PM

To cover my wife and me, it would cost us $12,311 per year - versus the approximately $4,200 its costs us now. The out-of-pocket would be a maximum of $12,700. That's for a silver plan.

The Bronze plan would cost us $9,048 per year, but would have higher out-of-pocket hurdles.

I don't qualify for a subsidy - nor for any tax breaks. Holy crap.

Luckily for me, I'm not being kicked out to the exchanges ... yet. If I ever am, I will need a $9,000 per year raise in salary just to keep the same level of disposable income.

I know my employer pays a portion of the actual overall premium, but not $9,000 per year.

The Republicans need to stop trying to delay this thing and let the full impact hit before the 2014 elections - so people will see what the real cost of electing the idiots who rammed this down our throats is - and maybe stop believing the "it won't cost you a thing" pipe dreams of bunch of out-of-touch socialists.

Conan the Grammarian at September 30, 2013 2:57 PM

I am 57. Husband is 55 and non smokers. We are both covered, but the price if we were not would be 17,221 a year

I think our portion of the FEHB is around 4000 a year right now. Of course, We also live in a state that opted out of the exchanges.

Isab at September 30, 2013 3:14 PM

We pay $11,608 now for COBRA and the calculator estimated $9,395 (silver) or $6,425 (bronze).

veacbhh at September 30, 2013 3:44 PM

28 year old out here in california on my own living just slightly over paycheck to paycheck... I'm actually one of the lucky ones and recieve coverage where I am working, but in the case that I do not, I am given the "Bronze Plan", Unsubsidized annual premium is $2,657, and I recieve no government tax credit subsidy.

Under this plan, it says it covers about 60% of out of pocket expenses, so with my medications, it could be higher.

Most people my age, or any age for that matter, cannot say that they have read this health care bill, I can say that I have read it. I was unemployed when it first came about and I had some time. I only focused on the small part about pre-existing conditions and I can tell you all, this bill will not help me if my life depended on it.

lil_tot at September 30, 2013 4:11 PM

A bronze plan is $3,803 claiming I have no employer coverage. My YTD employer health insurance cost is $919.68.

So I can keep my plan unchanged and my plan cost is going to go down? That's what Obama claimed.

Anonymous Coward at September 30, 2013 5:35 PM

"The Republicans need to stop trying to delay this thing and let the full impact hit before the 2014 elections - so people will see what the real cost of electing the idiots who rammed this down our throats is - and maybe stop believing the "it won't cost you a thing" pipe dreams of bunch of out-of-touch socialists."

The problem with that is, just from the responses, many won't see the change. Their employers will, and if employer drops it will look like evil corporations. Democrat supporters have gotten their wavers. And if they keep donating to the Dems they will continue to be waived. The young won't they are on their parents for 4 more years. By the time they actually pay, it will have failed and need to be replaced by worse.

Who will see the hit? Self insured will, majorly.

And since the numbers won't be close, taxpayers will. But how much of my tax bill will be due to this, who would be able to say.

Instead of trying to kill it, should support it with one stipulation, no waivers.

Joe J at September 30, 2013 5:48 PM

Annual Premiums - 2 adults, non-smokers, 50's. Not eligible for any subsidy.

Bronze Plan - $8492

Silver Plan - 10,530

Since I have coverage through my employer, I checked those rates.

My portion of premium under employer-sponsored plan - $2843.

The TOTAL premium under my employer-sponsored plan (my portion plus my employer portion) - $7943.

Remember, the PPACA is supposed to provide affordable health insurance. It's not the insurance that's affordable. It's the fact that it is subsidized.

Tasha at September 30, 2013 6:02 PM

Any reason we should believe this thing is accurate?

Patrick at September 30, 2013 6:22 PM

Just me: Had to say no employer insurance

bronze: 2613

silver: 3435 (which is about what I paid on Cobra in 2010)

I have a high deductible plan this year so I pa y nothing and my employer puts ~$500 into a FSA for me.

The Former Banker at September 30, 2013 6:45 PM

As Congress gets busted for declaring themselves immune from Obamacare, join us for this week's episode of

The Turning Worm

Gog_Magog_Carpet_Reclaimers at September 30, 2013 6:48 PM

It costs me zero since I'm covered by my employer. It sure won't cost me anything, it can only save me money. 20 years ago, our family premiums were $1760 (or was it 1780?) per month. I imagine they would be at least twice that if I had to cover myself today. No one is paying over $3,000 per month.

Jen at September 30, 2013 8:03 PM

Didn't use the calculator, but I got a notice from Kaiser which showed next year's rate, and it's going up $298 a month for me and my wife combined. Not all of that is due to Obamacare, because they do normally increase our rate a little every year, but I'm sure most of it is.

Rex Little at September 30, 2013 8:34 PM

Fortunately, for the moment (the job is looking shaky) our family of four is covered through my employer for about $5000/yr. Otherwise, we'd be on the hook for $12,700/yr for the Silver plan, or Bronze at $9,392. No subsidies, no tax breaks, and the Silver plan is worse coverage than we currently have. Costs as much as our house payment plus food for the month.

But if we kiss off the high-paying (and also high stress and demanding) jobs and go to work at min wage, we could get it for $1,965 with a $10K subsidy paid for by some sucker. Or we could just quit work entirely and sit at home to get Medicaid, EBT cards, Section 8, etc., paid for by that same sucker.

Looks like that whole "get an engineering degree and work hard and pay taxes and be a responsible citizen" thing just isn't going to pay off...for us.

Chuck at September 30, 2013 9:39 PM

"Any reason we should believe this thing is accurate?"

Is there any reason we should believe it isn't?

We're talking NPR here. Odds are pretty good that this calculator is weighted to make the costs less horrible than they might actually be.

It's not particularly likely that they're going to put these costs in the worst possible light, after all.

there are some who call me 'Tim?' at October 1, 2013 1:07 AM

Tim: Is there any reason we should believe it isn't?

Uh, Tim? When you come to me and tell me that this calculator will determine how much I will be paying for insurance under the Affordable Care Act, the assertion is on you; therefore, so is the burden of proof.

The rather basic fallacy you committed is known as "shifting the burden of proof," and it's pretty transparent. Maybe not as much as argumentum ad hominem, but still, a student of Logic 101 would be able to spot that.

Patrick at October 1, 2013 2:13 AM

Tim: Is there any reason we should believe it isn't?

Uh, Tim? When you come to me and tell me that this calculator will determine how much I will be paying for insurance under the Affordable Care Act, the assertion is on you; therefore, so is the burden of proof.

The rather basic fallacy you committed is known as "shifting the burden of proof," and it's pretty transparent. Maybe not as much as argumentum ad hominem, but still, a student of Logic 101 would be able to spot that.

Posted by: Patrick at October 1, 2013 2:13 AM

No need to argue about it Patrick. Just go onto the exchange, if they ever get it up and running and price a policy for yourself.

Then compare it to the table. Simple.

Isab at October 1, 2013 5:17 AM

Here are my results, based on a 55 year old non-smoker with one child, $22,000 annual income, no health insurance available from employer (working through a temp agency, part time).

Results

The information below is about subsidized exchange coverage. Note that subsidies are only available for people purchasing coverage on their own in the exchange (not through an employer). Depending on your state's eligibility criteria, you or some members of your family may qualify for Medicaid.

Household income in 2014:

142% of poverty level

Unsubsidized annual health insurance premium in 2014:

$11,317

Maximum % of income you have to pay for the non-tobacco premium, if eligible for a subsidy:

3.52%

Amount you pay for the premium:

$775 per year

(which equals 3.52% of your household income and covers 7% of the overall premium)

You could receive a government tax credit subsidy of up to:

$10,542

(which covers 93% of the overall premium)

Bronze Plan

The premium and subsidy amounts above are based on a Silver plan. You have the option to apply the subsidy toward the purchase of other levels of coverage, such as a Gold plan (which would be more comprehensive) or a Bronze plan (which would be less comprehensive).

For example, you could enroll in a Bronze plan for about $0 per year (which is 0% of your household income). By enrolling in a Bronze plan, you would receive $7,967 in subsidies, which would cover the entire amount of your Bronze premium. For most people, the Bronze plan represents the minimum level of coverage required under health reform. Although you would pay less in premiums by enrolling in a Bronze plan, you will face higher out-of-pocket costs than if you enrolled in a Silver plan.

Out of Pocket Costs

Your out-of-pocket maximum for a Silver plan (not including the premium) can be no more than $4,500. Whether you reach this maximum level will depend on the amount of health care services you use. Currently, about one in four people use no health care services in any given year.

You are guaranteed access to a Silver plan with an actuarial value of 94%. This means that for all enrollees in a typical population, the plan will pay for 94% of expenses in total for covered benefits, with enrollees responsible for the rest. If you choose to enroll in a Bronze plan, the actuarial value will be 60%, meaning your out-of-pocket costs when you use services will likely be higher. Regardless of which level of coverage you choose, deductibles and copayments will vary from plan to plan, and out-of-pocket costs will depend on your health care expenses. Preventive services will be covered with no cost sharing required.

Other Coverage Options

Children and young adults under age 30 are eligible to purchase catastrophic coverage. With a catastrophic plan, you would pay out-of-pocket for most health services until you reach the annual limit on cost sharing ($12,700 in 2014). However, preventive services are covered with no cost sharing required.

Children under the age of 19 may also be eligible for coverage under Medicaid or the Children's Health Insurance Program (CHIP), depending on your state's eligibility requirements.

FML.

Flynne at October 1, 2013 5:26 AM

I don't get any subsidy (because I decided I like to have money to pay outright for college, I work 60 plus hrs a week at two jobs, not including college), and my out of pocket expenses on the Bronze (which has a higher deductible than my current employer plan does in my state) would save me $50/month on premium, but again, at the cost of a $6500 deductible versus $5000 now. If I were to go to the Silver in my state, it would drop my deductible to $2500 and be $50 more per month than the equivalent plan at one of my employers (and since I work part time retail there, I can't be sure they won't drop me to the exchanges, although the Tax form regarding what they paid for my healthcare last year said they were just $150 over the $2000 employer penalty in what they paid for, so I don' know if they would drop me now, for two years, and then have to start paying for me in two years when the employer penalty goes up significantly. I guess it would save them lots of money to do that across all workers, but that really depends on how much more than the penalty everyone on the plan is, not just me, since I'm on the 2nd most basic tier.

spqr2008 at October 1, 2013 6:19 AM

If you're in California, this calculator also tells you what your co-pays, deductibles, etc. will be. I really wonder how all this is going to affect my health insurance through work. I don't imagine it's going to be very good.

https://www.coveredca.com/shopandcompare/

sara at October 1, 2013 6:44 AM

The two calculators came out very close for me with a Kaiser Silver 70 plan on the official Covered California calculator and a Silver plan on the NPR calculator.

So, I'm gonna say it's probably accurate.

Conan the Grammarian at October 1, 2013 8:30 AM

I put in what our income would be in the last place we lived in the US, Philadelphia, based on the job offer my husband had.

I didn't get a number, I got this:

Results

In general, employees who are offered insurance through work are not eligible for subsidized exchange coverage, so long as their insurance meets specified requirements. You would only be eligible for subsidized exchange coverage if your income is between 1 and 4 times the federal poverty level and you would have to pay more than 9.5% of your household income for your own coverage through the insurance offered by your employer.

NicoleK at October 1, 2013 11:25 AM

If we didn't have govt health care we would have to pay $8,746 out of pocket. No subsidies. It's pretty comparable to what we pay out-of-pocket here in Switzerland, give or take a couple hundred.

NicoleK at October 1, 2013 11:28 AM

Live in Oregon, household income $135,000. Two adult nonsmokers, 32 (me) and 35 (DH), three children under the age of 3. Calculator states we make 490% of the poverty level so no subsidy. Premium $8128 for exchange coverage which is far more than I pay now and far less coverage. My employer's insurance has 100% coverage after a $5 copay and $3 prescriptions, no deductible, family max out of pocket $1200. This is currently free as a benefit from my employer (Kaiser). They got an exemption through 2018.

BunnyGirl at October 1, 2013 11:36 AM

For additional fun, try calculating what your costs will be in 2, 5, or 10 years, assuming no price increase from today.

For our family of 4, (all non-smoking), it looks like we can look forward to about a $500 increase each year.

BerthaMinerva at October 1, 2013 12:52 PM

It would be $8,811 for our family of 4 non-smokers in Georgia. That's $2,000 more than we pay through our employer plans. We are not eligible for a subsidy, because it says we're 972% above the poverty level. The maximum out-of-pocket is $12,700 vs. $6,500 on the current plans. But then again, my employer has already made national headlines in its decision to drop part-time employees' coverage and raise premiums on everyone else. I'll find out this month how much more I'll have to pay. It doesn't sound like my costs are going down, B. O.! Can't wait!

KimberBlue at October 1, 2013 8:52 PM

836% of poverty level, so no subsidies.

Silver Plan:

Covers 70% of eligible expenses.

Don't know what the deductible would be.

$6350 maximum out of pocket.

$6907 estimated annual premium, according to Kaiser Foundation calculator.

$7212 estimated annual premium according to the Washington Health Benefit Exchange calculator.

Current plan through my employer, which includes coverage for dental and vision.

Covers 90% of eligible expenses.

$200 deductible.

$1750 maximum out of pocket.

$6500 annual premium, of which I pay $2470 and my employer pays $4030.

Ken R at October 2, 2013 12:00 PM

So, Patrick - have you figured out your problem?

I mean with the calculator, not supporting the Administration.

What is the difference in YOUR case?

I bet this will be interesting...

Radwaste at October 4, 2013 11:11 AM

Leave a comment